How to Work With Your Insurance Adjuster During a Fire Rebuild — And What Your Contractor Should Handle

The insurance process is one of the most stressful parts of rebuilding after the Palisades fires. Understanding who does what — and what your contractor should be managing on your behalf — can save months of frustration and thousands of dollars.

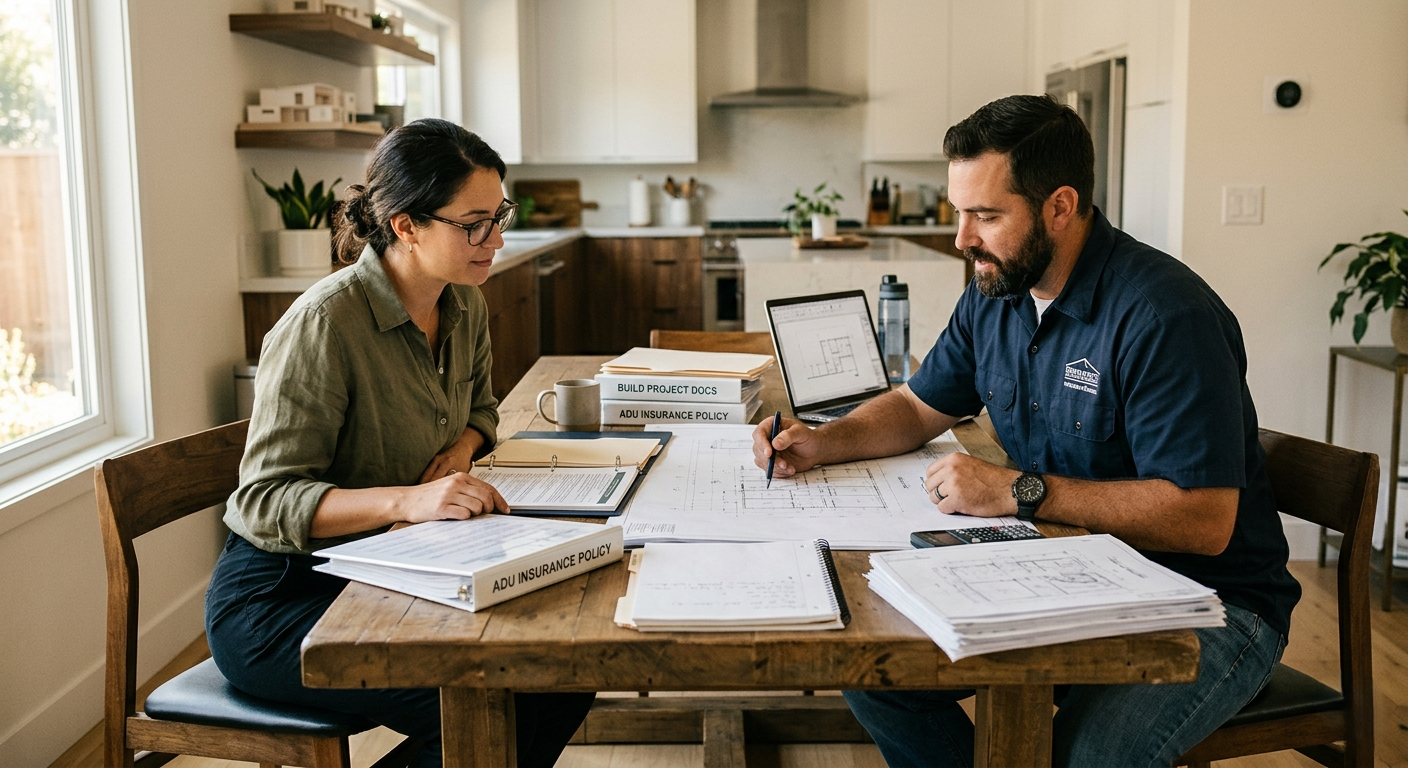

Most Palisades homeowners have never filed a total-loss insurance claim before. The process is simultaneously one of the most important and most opaque things you'll navigate during a rebuild — and the difference between a well-coordinated claim and a poorly managed one can be measured in hundreds of thousands of dollars.

A good fire rebuild contractor doesn't just build. Their project manager coordinates directly with your adjuster, provides itemized documentation, separates code-required upgrade costs, and supports supplemental claims. If your contractor is not doing this, you are leaving money on the table and managing a process that should be managed for you.

Understanding Who Your Adjuster Is

Before you can work effectively with your insurance adjuster, you need to understand which kind you're dealing with — because they have very different roles and incentives.

Insurance company adjuster (staff adjuster): Employed by your insurance company. Their job is to assess your loss and settle the claim. They are not adversarial, but they are paid by the insurer and will settle based on their documentation — not yours, unless you provide better documentation.

Independent adjuster: Hired by the insurance company to handle claims on their behalf. Same dynamics as a staff adjuster — they are working for the insurer, not you.

Public adjuster: Hired by you, the homeowner, to represent your interests in the claim. Paid a percentage of your settlement (typically 10–15%). Can be valuable for complex or disputed claims but adds cost. Not always necessary if your contractor is providing strong documentation.

What the Adjuster Is Evaluating

Your adjuster's job is to calculate the cost to rebuild your home to its pre-fire condition — and to identify any policy provisions that expand or limit that obligation. The key categories they evaluate are:

Dwelling coverage (Coverage A): The primary coverage that pays for rebuilding the structure. Most Palisades policies were significantly underinsured relative to 2025–2026 construction costs.

Other structures coverage (Coverage B): Covers detached structures — garages, guest houses, fences, retaining walls. Typically 10% of Coverage A.

Additional living expenses (Coverage D/ALE): Pays for temporary housing while your home is being rebuilt. This is the money paying your rent — and it runs on a clock.

Ordinance or law / code upgrade coverage: Pays the additional cost of bringing your rebuilt home up to current code standards — including 2026 WUI compliance. This is critical for Palisades rebuilds and frequently underutilized.

Personal property coverage (Coverage C): Covers your belongings. Separate from the dwelling and handled with a different documentation process.

"Code upgrade coverage — also called ordinance or law coverage — should pay for most WUI compliance costs on your rebuild. Most homeowners never explicitly claim it. Most adjusters won't volunteer it."

What Your Contractor Should Handle

A qualified fire rebuild contractor does not just build the home — they actively support the insurance claim process. Here is the division of responsibility that should exist between your contractor and you:

The Code Upgrade Conversation — Have It Before Construction Starts

The most important insurance conversation to have before your rebuild begins is about code upgrade coverage. The 2026 WUI code adds $9,000–$28,000 in required upgrades to most Palisades rebuilds — ember-resistant venting, Class A roofing, noncombustible cladding, fire-resistant glazing, noncombustible decking.

These costs are code-required. Your insurer's ordinance or law coverage should cover them. But you need to:

- 1

Confirm your policy includes ordinance or law coverage and understand the dollar limit. Some policies cap it at 10% of Coverage A, others at 50% or higher.

- 2

Have your contractor itemize all WUI costs separately in the estimate — not bundled into general construction costs. The adjuster needs to see these as distinct code-required line items.

- 3

Get written confirmation from your adjuster that WUI compliance costs will be covered under ordinance or law before construction begins. Not verbal — written.

Supplemental Claims — When the First Settlement Isn't Enough

Most initial settlement offers for Palisades fire rebuild homes are insufficient to cover the actual cost of rebuilding at current construction prices. This is not necessarily the adjuster acting in bad faith — initial estimates are often based on national cost databases that do not reflect actual Palisades market conditions in 2026.

Supplemental claims are formal requests for additional settlement funds when actual costs exceed the initial offer. They are common, expected, and legitimate. Your contractor should support supplemental claims by:

Providing detailed subcontractor bids that demonstrate actual market costs

Documenting material cost increases from the time of the initial estimate to the time of construction

Identifying scope items that were excluded from the initial estimate but are required by current code

Providing local comparable project data to support higher-than-average cost claims

Managing Your ALE Coverage

Additional Living Expense coverage pays for your temporary housing while your home is being rebuilt. It typically runs for 24 months from the date of loss — but some policies allow extensions for fire disaster situations. Key things to know:

Document every rental expense — keep all rental agreements, receipts, and payment records. The insurer reimburses actual expenses up to the policy limit.

Notify your adjuster if the rebuild timeline extends beyond your ALE coverage period. Many policies allow extensions for circumstances beyond your control — including permit delays. Request this in writing.

The ADU-first strategy under AB 462 effectively extends your ALE — by moving back to your property in an ADU, you stop the rent drain even if the primary home is not yet complete.

Keep ALE claims active even if you are making progress on the rebuild. ALE covers the period until the home is habitable — not just until construction starts.

Our project managers have worked with dozens of Palisades fire rebuild claims. We document everything, separate WUI costs, and support supplemental claims. Free consultation. CSLB License #982386.